How Did Section 24 Affect the Average Buy-to-Let?

For years, many UK buy-to-let investors relied on a fairly simple model:

- rental income,

- mortgage leverage,

- tax relief on interest,

- and long-term house price growth.

Then Section 24 changed the economics of the average buy-to-let.

For some landlords it reduced profitability significantly. For others, it completely changed how they structured deals.

What Is Section 24?

Section 24 refers to UK tax changes that restricted mortgage interest relief for individual landlords.

Before the changes:

- mortgage interest could usually be deducted fully before calculating taxable profit.

After the changes:

- landlords instead received a basic-rate 20% tax credit on finance costs.

This meant many landlords were suddenly taxed on figures much closer to turnover than actual cash profit.

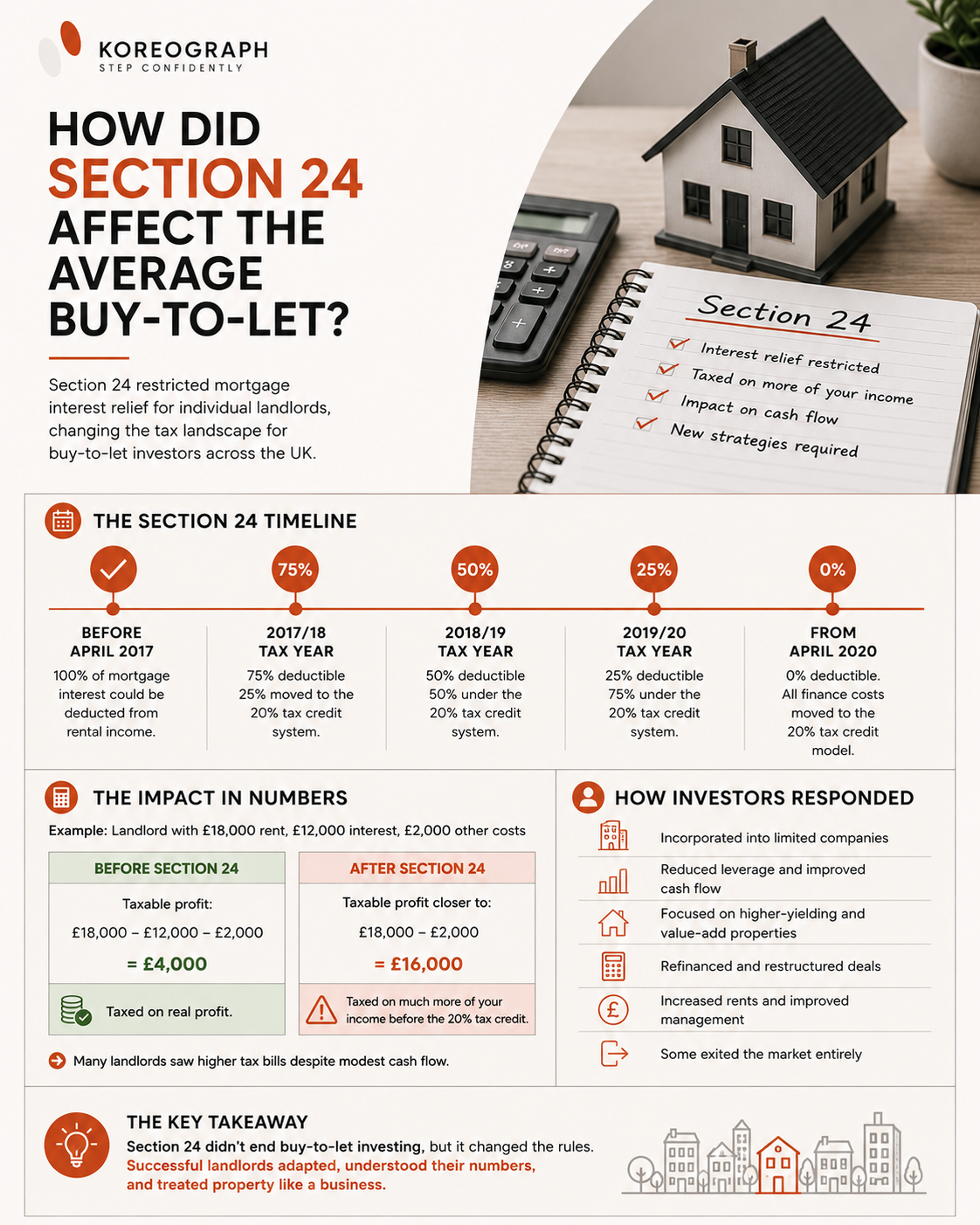

The Phase-In Timeline

The government introduced the changes gradually between 2017 and 2020.

Before April 2017

Landlords could deduct:

- 100% of mortgage interest.

2017/18

- 75% deductible

- 25% moved to the 20% tax credit system.

2018/19

- 50% deductible

- 50% under the tax credit system.

2019/20

- 25% deductible

- 75% under the tax credit system.

From April 2020

- 0% fully deductible.

- All finance costs moved to the 20% tax credit model.

Why Did This Matter So Much?

The impact was largest on:

- highly leveraged landlords,

- higher-rate taxpayers,

- portfolio investors,

- and interest-only borrowers.

A simplified example:

A landlord receives:

- £18,000 rent

Mortgage interest:

- £12,000

Other costs:

- £2,000

Before Section 24

Taxable profit:

After Section 24

Mortgage interest no longer reduced taxable profit in the same way.

The landlord could effectively be taxed closer to:

before receiving the limited tax credit adjustment.

For some landlords, tax bills increased dramatically despite relatively modest real-world cash flow.

How Investors Responded

Section 24 accelerated several major changes in the market.

Many landlords:

- incorporated into limited companies,

- reduced leverage,

- focused on higher-yielding deals,

- refinanced differently,

- increased rents,

- or exited the sector entirely.

SPV property companies became far more common because limited companies could still usually offset finance costs before corporation tax.

Why Incorporation Wasn’t a Perfect Fix

While company structures solved some issues, they also introduced:

- higher mortgage rates,

- more administration,

- additional accounting complexity,

- and potential SDLT or CGT issues when transferring existing portfolios.

For some investors incorporation made sense.

For others, it did not.

What Section 24 Really Changed

The biggest shift was psychological as much as financial.

Before Section 24, leverage was often viewed as an obvious advantage.

After Section 24, investors became far more focused on:

- cash flow strength,

- stress testing,

- debt exposure,

- and tax efficiency.

Property investing became less passive and more operationally analytical.

Final Thoughts

Section 24 did not kill buy-to-let investing.

But it fundamentally changed how many UK investors approach:

- leverage,

- portfolio structure,

- and long-term profitability.

The investors who adapted best were usually the ones who:

- understood their numbers,

- treated property like a business,

- and adjusted strategy rather than relying on old assumptions.